Key Takeaways

Q1: What is “How Can Employers Explain EPF How to Withdraw for Foreign Workers Clearly With 5 Simple Steps?” and why does it matter?

It is a practical employer guide for explaining EPF withdrawal categories, documents, channels, and follow-up steps to foreign workers, which matters because HR clarity reduces payroll confusion, compliance mistakes, and avoidable delays in Malaysia.

Q2: How does epf how to withdraw work for foreign workers in Malaysia?

For most foreign workers, the process starts by identifying the correct withdrawal type, such as Leaving Country Withdrawal or Akaun Fleksibel withdrawal, then checking eligibility, preparing supporting documents, and submitting through KWSP’s approved online or manual channels.

Q3: What should employers do next after learning epf how to withdraw?

Employers should create a simple internal SOP, brief HR and payroll staff, verify worker documents early, and direct staff to the correct KWSP channel, especially because non-Malaysian employees may face specific verification limits or office-visit requirements.

epf how to withdraw is a question many employers in Malaysia need to answer carefully, especially when foreign workers ask whether they can access EPF savings before leaving the country, during employment, or for approved account-based purposes.

For SMEs, startups, and companies without a full in-house HR team, this is not just an employee communication issue. It also affects payroll accuracy, document handling, exit management, and compliance confidence.

In practice, employers often face the same problems: staff do not know which EPF account applies, they confuse full withdrawal with partial withdrawal, or they assume every request can be completed online without verification.

Current KWSP guidance shows that foreign workers returning to their home country may apply for Leaving Country Withdrawal to withdraw all EPF savings, while Akaun Fleksibel (Account 3) withdrawals are also available under specific rules, including online limits for non-Malaysian employees.

This is where structured HR support matters. MUSTRE operates in Shah Alam as an HR outsourcing and consulting partner for Malaysian businesses that need stronger payroll, compliance, recruitment, and employee management systems.

That positioning is reflected in client feedback such as

Amir Munzir Mohd Salleh’s note that outsourcing HR helped his SME focus on core operations, and Dahlia Naz’s testimonial that MTR helped complete an updated employee handbook based on the 2024 Act.

Hire us!

Elevate your business with tailored HR solutions, including compliance, talent acquisition, culture building, and streamlined processes. Unlock success today!

These examples reinforce a practical point: when employers explain statutory processes clearly, staff management becomes more organized and less reactive.

This article breaks the topic into 5 simple steps so employers can explain EPF withdrawal options for foreign workers with greater accuracy, fewer misunderstandings, and better HR control.

What Does EPF How to Withdraw Mean for Foreign Workers in Malaysia?

Employers can explain epf how to withdraw for foreign workers by matching the worker’s situation to the correct KWSP withdrawal type, required evidence, submission channel, and verification method under current Malaysian EPF rules.

Why Employers Need to Explain EPF Withdrawal Clearly to Foreign Workers

Clear employer guidance matters because foreign workers often depend on HR, payroll, and admin teams to interpret KWSP categories, avoid document errors, and understand whether a withdrawal can be done online or only at the counter.

For SMEs and startups, this is more than a benefits question. It affects final payroll coordination, work pass timing, departure planning, and employee confidence. When employers give vague answers, workers may submit the wrong request, miss required evidence, or assume that every EPF transaction is fully digital.

Who Qualifies for EPF Withdrawal as a Foreign Worker

Foreign workers may qualify for different EPF withdrawal routes depending on whether they are returning to their home country, still employed in Malaysia, below age 55, or withdrawing from a specific EPF account.

KWSP states that expatriates, permanent residents, and foreign workers returning to their home country can choose to withdraw all EPF savings under Leaving Country Withdrawal. That is the clearest full-withdrawal pathway employers should explain in exit-related cases.

EPF How to Withdraw for Employees Returning to Their Home Country

Foreign workers returning permanently to their home country can generally be guided toward Leaving Country Withdrawal, which is the clearest full-withdrawal route employers should explain during exit planning and final HR documentation.

Employers should explain that this is not the same as a normal partial withdrawal. It is usually tied to the worker’s departure from Malaysia, so HR should help check passport details, employment end records, bank account readiness, and any supporting documents needed before the employee starts the application.

EPF How to Withdraw for Workers Still Employed in Malaysia

Foreign workers who are still employed in Malaysia usually need to check whether their request falls under a partial withdrawal category such as Account 2 or Account 3, rather than assuming they can withdraw all EPF savings.

This is where employers need to be precise. If the employee is not leaving Malaysia permanently, HR should first identify the reason for withdrawal, then match it to the correct account and current KWSP conditions. That prevents confusion between flexible access, approved-purpose withdrawals, and full leaving-country claims.

Which EPF Accounts Should Employers Explain Before Any Withdrawal?

Employers should explain Account 1, Account 2, and Account 3 first because withdrawal approval depends on the account involved, the worker’s purpose, and whether the request is a full exit withdrawal or a partial statutory withdrawal.

What Employers Should Know About Account 1, Account 2, and Account 3

Each EPF account serves a different savings purpose, so employers should never tell workers to “just withdraw EPF” without clarifying which account applies and whether the reason is actually recognized by KWSP.

Account 3, also known as Akaun Fleksibel, is meant for more accessible savings and can be withdrawn when the account has at least RM50. Payments, once processed and approved, are credited directly into the member’s bank account, making this the most practical partial-withdrawal example for employers to explain.

How to Withdraw EPF Account 2 for Approved Needs

Employers should explain that Account 2 withdrawals are usually tied to specific approved purposes, so foreign workers should not assume they can use this account freely for any personal financial need.

The safer HR approach is to confirm the employee’s reason first, then check whether the request matches a recognized EPF category. This helps employers avoid overpromising, reduces document mistakes, and keeps withdrawal guidance aligned with the proper account purpose.

How EPF Account 3 Withdrawal Works for Flexible Access

Employers should explain that Account 3 is the more flexible EPF account, which makes it easier for eligible members to access savings compared with more restricted withdrawal categories.

For foreign workers, this explanation must still come with caution. HR should remind employees that flexible access does not mean unlimited access, because eligibility, minimum balance, transaction limits, and verification requirements can still affect whether the withdrawal is processed smoothly.

Why Account Type Matters Before Starting Any EPF Withdrawal Request

Account type matters because the wrong category leads to the wrong form, wrong expectation, and wrong supporting documents, which can delay processing and create unnecessary HR back-and-forth.

This is especially important when a worker says the money is needed for “personal use.” Employers should not treat that phrase as a valid withdrawal category on its own. Instead, they should check whether the request fits Account 3 access, a recognized Account 2 purpose, or Leaving Country Withdrawal.

How Does EPF Account 3 Withdrawal Affect Foreign Workers?

EPF Account 3 withdrawal gives foreign workers a flexible option in certain cases, but employers must explain the transaction limits and channel restrictions that may apply to non-Malaysian members.

What Is EPF Account 3 Withdrawal and When Can It Be Used?

EPF Account 3 withdrawal allows eligible members with savings in Akaun Fleksibel to withdraw at any time, subject to minimum balance and channel conditions set by KWSP.

KWSP states that Akaun Fleksibel withdrawals can be made once the account has a minimum of RM50. Payments, once processed and approved, are credited directly into the member’s bank account, making this the most practical partial-withdrawal example for employers to explain.

EPF How to Withdraw Through Account 3 for Non-Malaysian Employees

Employers should explain that non-Malaysian employees may use Account 3 for flexible withdrawal only when their EPF account status, identification details, and submission method meet the current EPF requirements.

This is where HR communication must stay precise. Foreign workers should be told to verify their eligibility first, use the correct EPF channel, and prepare for possible extra verification if the application cannot be completed smoothly through the standard digital process.

Minimum Amount, Eligibility, and Withdrawal Channels

Minimum amount, eligibility, and withdrawal channel are the three checks employers should explain first because they determine whether an Account 3 request can proceed quickly or needs further review.

A practical HR explanation is simple: confirm that the employee has sufficient balance in the correct account, confirm that the withdrawal type is allowed, and then direct the worker to the proper EPF submission route, whether digital or manual. This reduces confusion and helps employees avoid avoidable rejection or delay.

When Employers Should Recommend Account 3 Instead of Other Withdrawal Options

Employers should mention Account 3 when the worker is not leaving Malaysia permanently, needs flexible access to eligible savings, and meets the current account and verification requirements.

At the same time, employers must explain a crucial limitation: KWSP says online applications for non-Malaysian employees are limited to a maximum of RM3,000 per transaction for Akaun Fleksibel, and other cases may require manual counter handling.

Can Foreign Workers Use EPF Withdrawal for Personal Use?

Foreign workers may use EPF withdrawal for personal use only when that “personal use” fits an actual KWSP withdrawal category, because EPF approval depends on rules, not on general financial preference.

What EPF Withdrawal for Personal Use Really Means

EPF withdrawal for personal use usually means the worker wants accessible funds, but employers should translate that request into a compliant category such as Account 3 access or an approved Account 2 purpose.

Good HR communication here is simple: do not promise approval based on the employee’s explanation alone. Check the purpose, the account, the supporting records, and whether the worker’s status involves leaving-country withdrawal instead of an ordinary in-service request.

How Employers Can Avoid Giving Misleading Advice About Personal Use

Employers can avoid misleading advice by using a checklist that separates withdrawal reason, EPF account, submission channel, and required documents before giving any answer to the employee.

That checklist approach fits MUSTRE’s service model well because payroll, HR administration, training, and Corporate Compliance and Officer Management all rely on structured processes rather than ad hoc verbal guidance. MUSTRE presents itself as a provider of HR management, payroll management, and consultation services for smoother company operations.

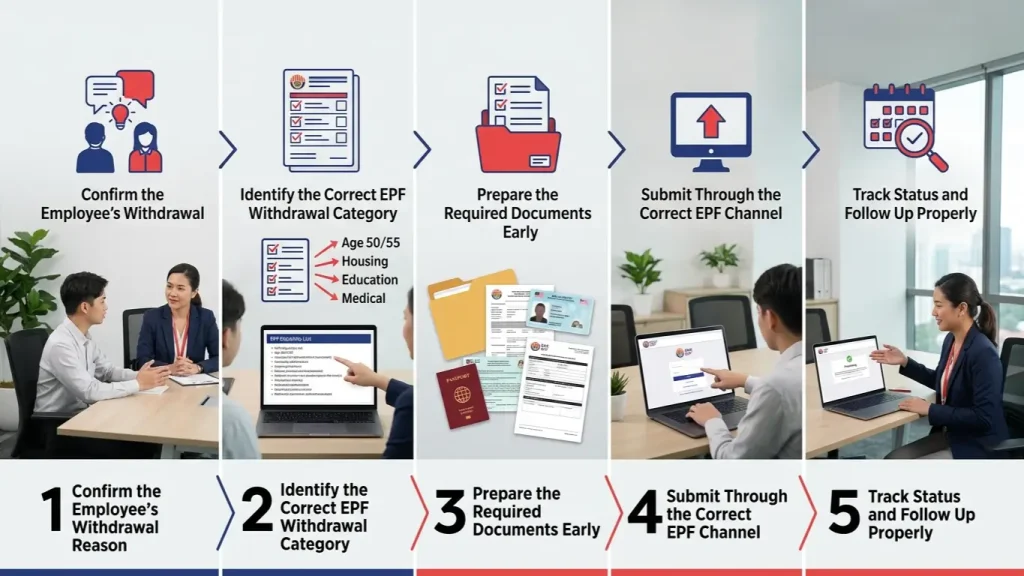

What Are the 5 Simple Steps Employers Can Use to Explain EPF How to Withdraw?

Employers can explain EPF withdrawal clearly by using a five-step method: confirm the reason, identify the category, prepare documents, submit through the right channel, and track the status until completion.

Step 1: Confirm the Employee’s Withdrawal Reason

The first step is to confirm exactly why the worker wants to withdraw, because the reason determines whether the case involves Leaving Country Withdrawal, Account 2, or Account 3.

Step 2: Identify the Correct EPF Withdrawal Category

The second step is to classify the request properly, since full withdrawal and partial withdrawal are not processed the same way by KWSP.

Step 3: Prepare the Required Documents Early

The third step is to collect identity, work-pass, banking, and purpose-based documents early, because incomplete evidence is one of the most preventable sources of delay.

Step 4: Submit Through the Correct EPF Channel

The fourth step is to submit through the correct channel, whether that is the KWSP i-Akaun app, the member portal, or a physical EPF office.

Step 5: Track Status and Follow Up Properly

The fifth step is to track the application and explain possible verification delays, especially for non-Malaysian members whose transactions may be limited online or routed to manual handling.

What Documents Are Required for EPF Withdrawal by Foreign Workers?

Foreign workers usually need identity, banking, and case-specific supporting documents, and employers should remind them that leaving-country cases may require proof tied to passport and status records.

Basic Documents Employers Should Ask Workers to Prepare

Basic preparation normally includes passport details, bank account information, and other records needed to match the member’s identity with EPF records accurately.

Additional Documents Based on the Withdrawal Type

Additional documents depend on the withdrawal type, so employers should not recycle one checklist for every request involving foreign staff.

For example, leaving-country applications may require supporting proof linked to nationality, exit status, or passport record differences, while account-based withdrawals depend more on eligibility and transaction conditions.

That is why one standard HR script is not enough without category-specific guidance, especially for employers handling expatriate and pass-related processes through Commercial Officer Hiring Services.

What Common EPF Withdrawal Mistakes Should Employers Help Foreign Workers Avoid?

The most common mistakes are confusing account types, assuming everything can be done online, and submitting incomplete documents without checking the exact KWSP route first.

Confusing Full Withdrawal, Account 2, and Account 3

Employers should correct this confusion early because each route has different rules, timelines, and employee expectations.

Assuming Every Request Can Be Approved Online

This assumption is risky because KWSP states that non-Malaysian members may face online limits or be required to apply manually at an EPF office for certain withdrawals.

Employers do not need to make EPF withdrawal explanations complicated for foreign workers.

The key is to match the worker’s situation to the correct withdrawal category, explain the right account clearly, prepare the required documents early, and set realistic expectations about online limits and verification.

When HR communication is structured, employers reduce confusion, protect compliance, and help employees handle EPF matters with more confidence.

If your company needs clearer support for foreign worker HR processes, payroll coordination, and statutory communication, MUSTRE can help you organize these issues more professionally.

From day-to-day HR administration to expatriate-related documentation support, MUSTRE gives SMEs and growing businesses a more structured way to manage staff matters.

Explore Commercial Officer Hiring Services to see how your team can handle employer obligations with less confusion and better control.

FAQ

How to withdraw EPF savings online in Malaysia

Employers should explain that online EPF withdrawal depends on the withdrawal category, the employee’s eligibility, and whether the worker can use the official EPF digital channel for that specific request.

For foreign workers, this is especially important because not every case is fully online from start to finish. The best approach is to confirm the reason for withdrawal first, then guide the worker to the right EPF channel, prepare documents early, and remind them that some cases may still require additional verification.

What documents are required to withdraw EPF funds

The required documents usually depend on the withdrawal type, but employers should start with a practical checklist that includes identity details, passport information, bank account details, and any supporting records tied to the employee’s request.

If the foreign worker is leaving Malaysia, the case may need additional proof connected to departure or status changes.

A simple HR checklist reduces delays, helps payroll teams stay aligned, and avoids repeated back-and-forth with employees.

EPF withdrawal process for foreigners working in Malaysia

The EPF withdrawal process for foreigners working in Malaysia should be explained in a sequence that is easy for employees to follow. First, confirm why the worker wants to withdraw.

Next, identify whether the request involves full withdrawal, Account 2, or Account 3.

Then prepare the documents, choose the right submission channel, and follow up on the application status.

This step-by-step explanation helps employers avoid giving unclear advice and helps workers understand what to expect.

How to track EPF withdrawal status online

Employers should tell workers to monitor their withdrawal status through the official EPF channel used for the submission, while also reminding them that not every delay means a rejection.

Status checks are useful because they help employees confirm whether the application is being processed, pending verification, or needs additional action.

For HR teams, encouraging workers to check status properly can reduce unnecessary follow-up questions and keep communication more organized.

Differences between full and partial EPF withdrawal options

Full and partial EPF withdrawals should never be explained as if they are the same process.

Full withdrawal is generally linked to a major status-based event, such as a foreign worker returning to the home country, while partial withdrawal is usually tied to specific accounts and approved access conditions.

Employers who explain this difference clearly will help staff avoid choosing the wrong route and improve the quality of supporting documents from the start.